Every fintech cost guide quote $50,000–$500,000 — all at US or Eastern European rates, none mentioning India. The architecture decision that matters more than any feature: Banking-as-a-Service, or your own money transmitter license. Here’s the honest version of both.

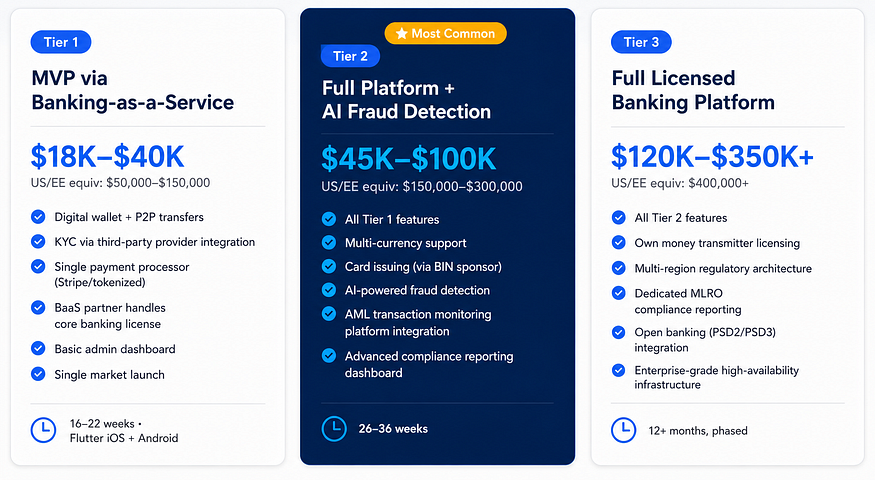

The number you came here for Fintech app development like PayPal or Cash App costs $18,000–$40,000 for an MVP (digital wallet, peer-to-peer transfers, KYC via a third-party provider, single payment processor) at India development rates using a Banking-as-a-Service partner. A mid-tier platform with multi-currency support and AI fraud detection costs $45,000–$100,000. A full banking-style platform with its own licensing costs $120,000–$350,000+. US and Eastern European agencies quote $50,000–$500,000+ for the same scope — and none of them mention India rates as an option. Compliance work alone typically accounts for 20–40% of any fintech app’s budget, regardless of who builds it. Get a free fintech app estimate →

Fintech app development is the one app category where the architecture decision genuinely outweighs every feature decision combined. You can scope a beautiful wallet UI, a slick transfer flow, and a clean transaction history screen — and none of it matters if you haven’t decided, before any of that, whether you’re operating under someone else’s banking license or pursuing your own. That single choice determines your timeline, your regulatory exposure, and a meaningful share of your total budget, and it’s the part every generic “fintech app cost” article either skips or buries under a wall of compliance acronyms.

We’re also going to say something plainly that every competitor quote in this category avoids: India rates apply to fintech app development the same way they apply to every other app category. The compliance work itself — PCI-DSS scoping, KYC integration, AML monitoring — costs roughly the same in absolute terms wherever you build, because it’s largely third-party vendor fees and audit costs. But the engineering hours to implement it correctly cost 60–70% less at Indian rates than at US or Eastern European rates, and that gap compounds across a project where compliance alone can be 20–40% of the total.

$324B

Global fintech market by 2026

70%

Compliance & Security Risks

$18K

BaaS MVP Cost (India)

20–40%

Share of compliance budget

60–80%

BaaS avoids licensing

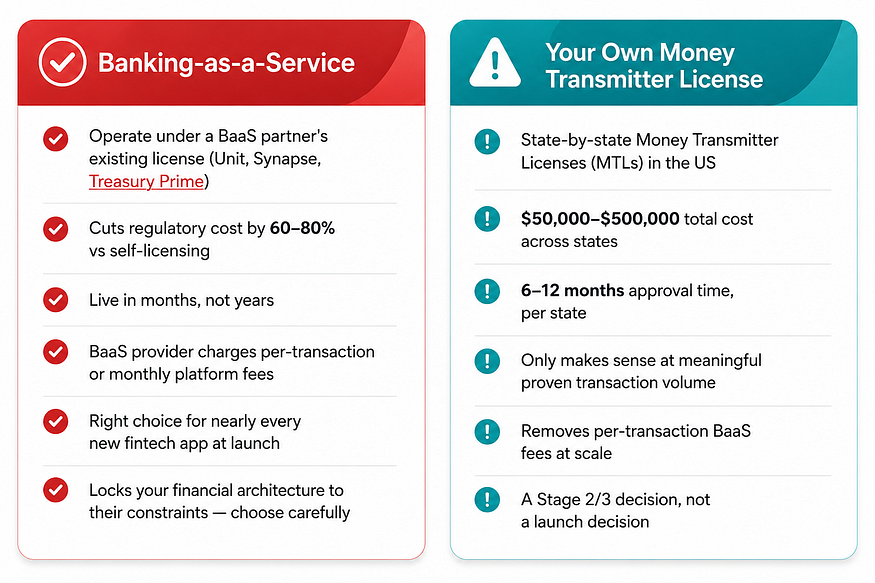

Banking as a Service vs Own License: The #1 Fintech App Decision

This is the conversation that should happen before a single screen gets designed for your payment app development project. Get this wrong and you either burn six to twelve months waiting on state-by-state licensing approval before you can legally launch, or you over-invest in licensing infrastructure for a product that hasn’t yet proven anyone wants it.

Why this decision locks in for years, not months: Choosing a Banking-as-a-Service partner isn’t just a vendor selection — it determines your financial network architecture for as long as you’re built on top of it. Different BaaS providers have different constraints around supported transaction types, geographic coverage, and integration depth. Evaluate this the way you’d evaluate a co-founder, not a software subscription, because migrating BaaS providers after launch is a genuinely painful, months-long project. Most founders should still choose BaaS over self-licensing at launch — the point is choosing the right BaaS partner deliberately, not skipping the decision.

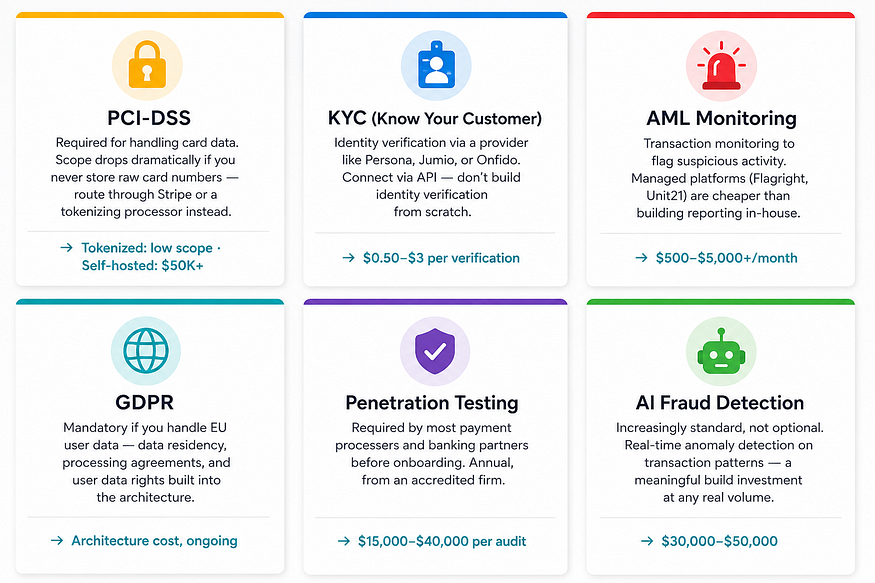

PCI DSS, KYC & AML Fintech App Compliance — Cost & What You Need

PCI DSS compliant app development isn’t a feature you add — it’s structural engineering that has to be designed in from the architecture stage, not retrofitted later. Retrofitting PCI-DSS compliance after launch costs three to four times more than designing for it up front, because by then it’s woven through code that wasn’t written with audit trails and data isolation in mind.

The compliance budgeting mistake that kills fintech projects mid-build: Treating compliance as the last 10% of the project rather than baking it into the architecture from the start is the single most common — and most expensive — mistake fintech founders make. A founder who scopes a beautiful feature list, then discovers mid-build that the data model doesn’t support proper audit logging, ends up rebuilding core infrastructure rather than adding a feature. Scope compliance architecture in week one, alongside your first wireframe, not after.

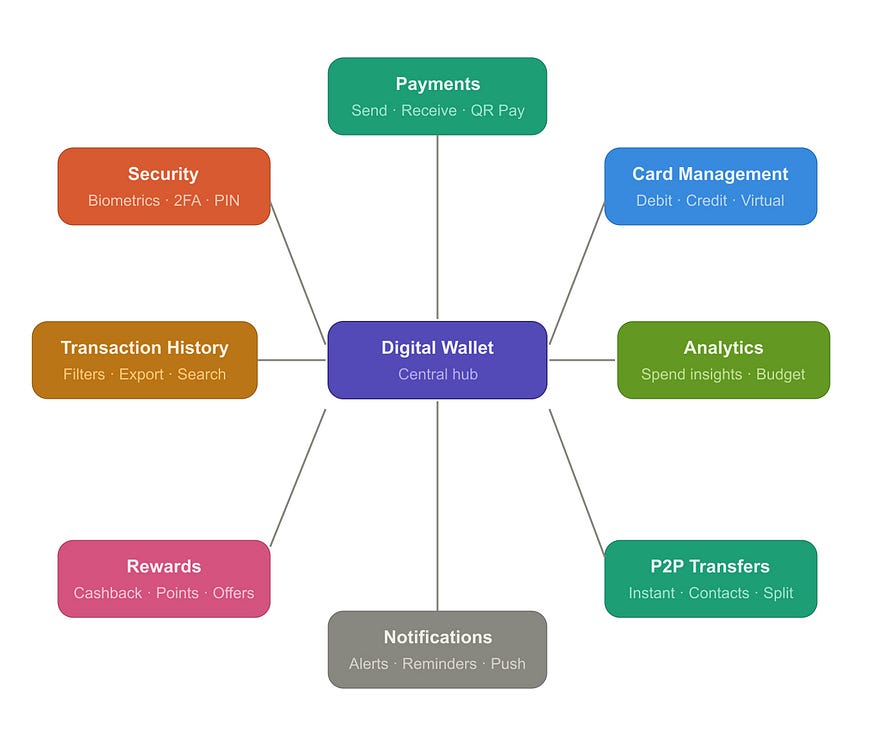

Digital Wallet App Features That Actually Matter in 2026

Core Payment App Features (Must-Have)

Digital wallet with real-time balance and transaction history. Peer-to-peer transfers with phone number or username-based recipient lookup. Bank account linking (via Plaid or a regional equivalent) for funding and withdrawal. QR code payments for in-person transactions. Biometric authentication (Face ID/Touch ID) as the default login method, not an optional add-on. Push notifications for every transaction, in real time, with no exceptions — this is a trust feature, not a convenience one.

KYC AML Compliance Features

KYC onboarding flow integrated at signup, not bolted on later. Transaction limits tied to verification tier (unverified users get lower limits, fully verified users get higher ones — a standard pattern across PayPal, Cash App, and Venmo). Dispute and refund request flow with clear status tracking. Account freeze/lock capability for the admin team when fraud is suspected, with a fast unlock path for false positives.

Admin Dashboard & Operations

Real-time transaction monitoring dashboard. KYC review queue for manual escalations that the automated provider couldn’t resolve. AML alert management with case notes and resolution tracking. Compliance reporting exports formatted for regulatory submission. Customer support tools with full transaction history visibility for resolving disputes quickly.

Why transaction limits tied to verification tier matter more than they look like they should: This single pattern — unverified users capped at low transfer amounts, fully KYC-verified users unlocked for higher limits — is simultaneously a compliance control, a fraud mitigation tool, and a genuine growth lever. It lets you onboard users instantly without requiring full KYC at signup (reducing friction and drop-off), while still satisfying regulatory requirements before meaningful money moves. Get the tier thresholds right and you improve both your compliance posture and your activation rate at the same time — get them wrong and you either create unnecessary friction or unacceptable regulatory exposure.

Fintech App Development Cost 2026–3 Tiers at India Rates

Fintech app development costs in 2026 vary by complexity. At India-based development rates, MVPs start around $25,000, while advanced fintech platforms with compliance, AI, and payments can exceed $150,000.

Flutter Fintech App Tech Stack — Built for Audit Trails

Why Flutter is a genuine fintech consideration, not just a general preference: Flutter’s compiled Dart code and Skia rendering engine give it a smaller attack surface than frameworks that lean on platform web views for parts of the UI, which matters for a category where every screen potentially touches sensitive financial data. The trade-off worth knowing: because Flutter draws every pixel itself, a developer building a card-entry field must explicitly ensure that content never passes through the rendering canvas in plaintext — a non-obvious PCI requirement that an inexperienced team can miss. This is exactly the kind of detail where fintech-specific development experience prevents an expensive mistake rather than just a generic engineering preference.

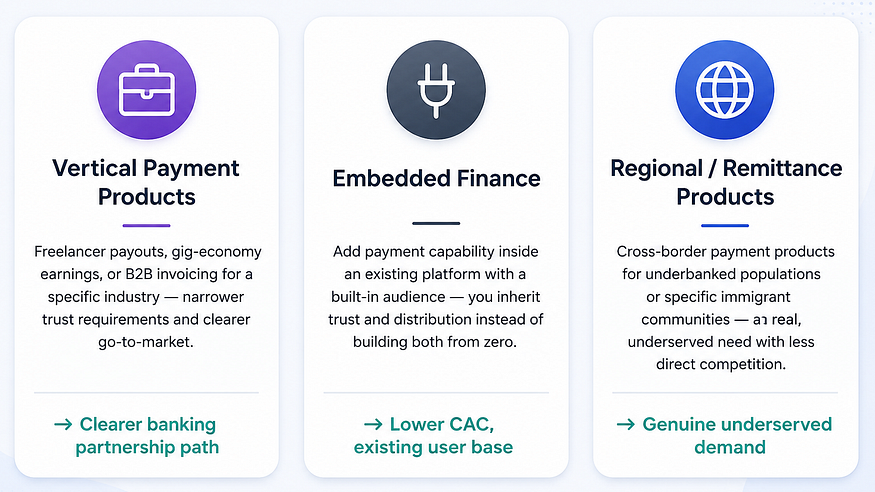

Best Niche Fintech App Strategy — What to Build Instead of PayPal

PayPal and Cash App have hundreds of millions of users, established banking relationships built over decades, and a level of regulatory trust a new fintech app development entrant cannot replicate quickly. A general-purpose consumer payment app trying to compete head-on is fighting a battle with no realistic path to winning the trust and scale these platforms already have.

“The founders who succeed in fintech in 2026 aren’t trying to out-PayPal PayPal. They’re solving a payment problem for a specific group of people that PayPal has no commercial reason to solve well — and that’s a fundamentally cheaper, faster path to a real banking partnership.”

Primocys · Fintech App Development

We Build Compliance In From Day One — Not Retrofitted Later

Primocys has shipped fintech products with HIPAA, PCI-DSS, GDPR, RBI, and SOC 2 compliance requirements built into the architecture from the first sprint, not added afterward. Flutter mobile apps, fixed price from $18,000, full source code.

Honest BaaS vs licensing scoping

We’ll recommend the right architecture for your stage — not the most expensive one.

KYC/AML integration done right

Persona, Jumio, or regional equivalents wired in correctly from the first sprint, not bolted on.

PCI-DSS scope minimised by design

Tokenized payment flows that never touch raw card data — the right architecture from day one.

Niche-first strategy advice

We’ll help you scope a vertical or embedded model with a real path to a banking partnership.

Flutter — compliance-aware build

Clutch Top Flutter Developer 2024 & 2026. PCI-aware rendering, biometric auth done correctly.

Fixed price from $18,000

Cost agreed before development starts. Milestone payments. Full source code ownership.

Conclusion: How to Choose the Best Fintech App Development Company in India

Building a fintech app like PayPal or Cash App in 2026 is entirely achievable — but only if compliance is treated as architecture, not an afterthought. The founders who succeed aren’t the ones with the longest feature lists; they’re the ones who made the BaaS vs licensing decision correctly before writing a line of code, scoped KYC/AML into the first sprint, and chose a payment app development company that has shipped compliant fintech products before — not one learning compliance on your budget.

India-based fintech app development delivers the same PCI-DSS, KYC, and AML compliance architecture at 60–70% lower engineering cost than US or Eastern European agencies. The compliance vendor fees — Persona, Stripe, Flagright — are identical globally. What changes is the engineering cost to wire them in correctly. That gap is where the real saving is, and for a $45,000–$100,000 Tier 2 platform, it’s the difference between a fundable MVP and a budget that ran out before launch.

The single most important step before you hire a fintech app development company: Tell us your target market, your business model, and your compliance requirements. We’ll give you an honest BaaS vs licensing recommendation and a fixed-price estimate broken down by feature and compliance component — within 48 hours, no commitment required. Get your free fintech app estimate →

Ready to Build Your Fintech App — Compliance Done Right From Day One

Tell us your target market and your business model. We’ll give you an honest BaaS vs licensing recommendation and a fixed-price estimate within 48 hours.